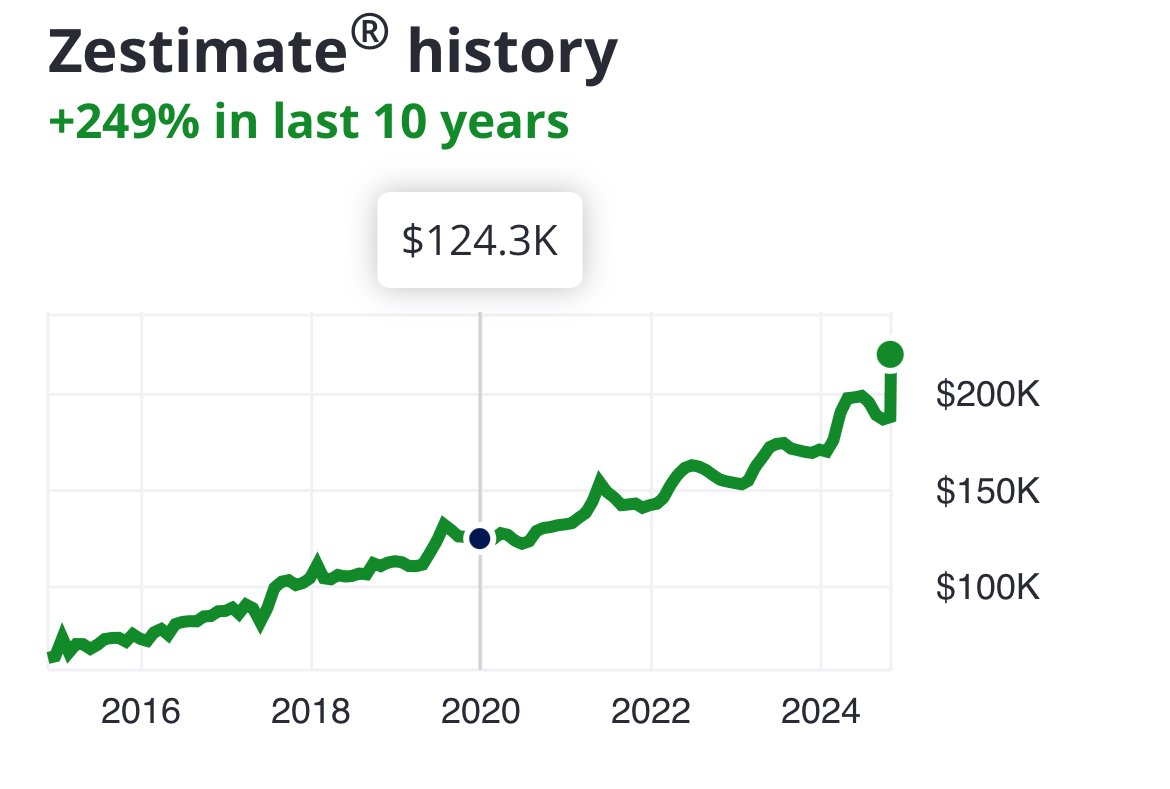

Houses in my area increases 82% in just 4 years

Houses in my area increases 82% in just 4 years

My salary didn't change at all, but homes went up 82%. The money I saved for a down payment and my salary no longer are good enough for this home and many others. This ain't even a "good" home either. It was a 200k meh average ok home before. Now it's simply unaffordable

You just need to stop watching Netflix and buying avocado toast.

At least that's what old people say anyway.

Can confirme. I stopped drinking Starbucks and now I own a 50 acre plot with a 6 bedroom house on it. If only I would have listened to their Facebook comments sooner, I could have afforded that private jet too. Edit: Apparently sarcasm is lost on a few. So for explicitness - /s

Assuming you spend $10 on avocado toast every day, as well as $75 on eating out for every meal, $20 for Starbucks, and ALSO assuming you have $150 worth of monthly subscriptions:

It will take you 25 years to save one million dollars. That's assuming you never get sick, never lose a job, never need to buy a car or have major repairs, or basically any kind of surprise expense or setback that could wipe out savings.

To be the richest person on earth, you would need to save that money every year for over 6 MILLION YEARS

Not to devalue your point, but if you truly were spending (10 + 3*75 + 20)*30 + 150 per month (so a total of 7800 USD) and you invest it in an index fund getting back 5%, you'll have your million in 10 years. 8 years at 10% which is the long-term growth rate of DJIA and S&P 500.

You'll still never be the richest person in the world, but if you truly were burning away that much money, you could make decent dough just from investing it passively. In 30 years you'd have like 15 million, more than enough to retire.

Now the only real problem is that nearly nobody is actually burning that much cash and the "stop eating avocado toast" suggestions are indeed stupid af.

A house in Austin

2018: $275,000

2022: $725,000Those are actual numbers from East Austin. I believe the 2024 market rate is $625,000 but it hasn't changed hands again so I can't say for certain.

And conservative Texans keep laughing that californians are moving to Texas because "They hate the blue politics", never guessing that they would bring their blue politics and money with them, driving up land value. Definitely not saying that they're bad, but that it's ironic that they didn't think through the consequences

The people fleeing California for Texas aren't people who love California and its politics.

They're mostly Republicans, and they're making Texas more red AND increasing home prices.

Is this one of the areas where corps are buying up a shitload of real estate?

I believe it's on earth, yes.

My moon base is not gaining ANY land value....

If it's on Zillow then yes. The trick is to find houses that are not on MLS/Zillow...but realistically there are none. GL! We got ours wnd in one year it went up 40%in a year.

Also in my area that house is a steal and would have offers before it hit Zillow.

At only 82% I'm going to say no.

I like the utility feed hanging off the front of the house going straight through the roof and blocking them from installing the other fake shutter. I wonder what other construction horrors lurk inside.

My lucky ass bought a house in late 2019. I'm happy I'm making money on it but this doesn't seem healthy

You're only making money if you downsize, move somewhere cheaper, or switch back to renting. If you move and all the other houses have gone up, then you just end up having to sink any gained equity into affording your new place. Rising prices really only help developers, realtors, and REIT's.

Exactly.

Right but you then control the appreciation on a much larger asset. In terms of pure net worth and net present value, trading up is a huge gain even if it doesn't generate more short term liquidity.

You can also rent out the smaller place and get both cash flow and NPV upgrade.

It is theur business to make money off it.

I am not sure how people living in house got convinced that they are now investors though

You're right. It's not healthy to profit so much from corporations greed.

Therefore, it's only right that you sell me your house for $1

I, too, would like a house for $1 please

Same here. And my stupid ass father in-law spread the rumor that we wanted to sell and we instantly had several offers. But we like it here.

We got in on on our house in early 2016 and the price of real estate in our area increased by 20% while we were in escrow.

Our house has more than doubled in price since then but if we had fallen out of escrow, we would not have been able to buy anything anywhere near our jobs/preferred city (and my partner and I have a combined income north of 150k/year).

Shit is crazy these days

With you there. Didn't realize how lucky we were, and honestly thought about waiting just one more year on multiple occasions. What's done is done, all I can do now is not feel guilty I got in, but rather just make the most of it. Pay off as quickly as I can, and vote to help others afford houses too.

Well you are set so luckily it doesn't affect you much in theory. If it crashes so be it as you probably aren't in a hurry to move.

Time to eat the rich

Best hurry ... Ozempic is destroying the caloric benefit

82%, feel lucky. I bought my house in 2015 for $85k. Last assessment was almost $300k

I keep thinking that it would be a great time to sell but then I realize there isn't a lot of other worth while places to go.

Unless you are ready to move to dead mans land

When the stock market doesn't perform as much as a fundamental need

Tbh this is more than mildly infuriating...

That you don't understand the realestate market? Or you didn't know this has been projected for a decade now from millennials getting as old as the avg age of first time home buyers and being the largest % share of the US population creating more demand than available supply?

This is everywhere. I've been looking for houses for 3 months in NW Ohio. 300k is the new 150k, and all the houses are beat to shit on the inside needing 50k just to make them passable inside because nobody takes care of them.

I wonder what proportion of it is also due to people fleeing 1 million + average house markets during the pandemic work from home wave. Not saying this about you, but it makes me think it's funny how the common refrain of "Don't like it? Just move" is often uttered by NIMBYs.

Friend of mine was saving up for a house 5 years ago. Prices have gone up almost 150%

Yeah that was me too... I FINALLY got to the point where I could realistically start looking, got the pre-approval and everything just after COVID started... People had already starting WFH and moving away from where they worked and investment companies kept buying and now I'm still living in someone else's garage because prices went through the roof pretty much as I was looking...

Of course once you mention WFH everyone gets defensive and claims this was a trend, but those charts are the same everywhere. Houses in 2018-19 were often less than half of what they cost now...

WFH is a logical thing to imagine, but there's a simpler trend that can be seen by looking at two graphs:

https://fred.stlouisfed.org/series/M2SL

https://fred.stlouisfed.org/series/MSPUS

"Please don't melt the economy" printing press fired up in 2020 and real estate investors seemed to get plenty of that cash. While inflation didn't quite match the M2 injection, anything "investment" like saw that bump. The M2 injection was enough to save the stock market, but housing, which did not see the same crash as stocks, got the same boost.

This is why, more than ever, people see that individuals almost don't get to participate and big companies are instead buying the stuff and maybe letting people rent them if they feel so inclined. The big companies got the boon of the M2 and most individuals got a modest bump by comparison.

Only 37 more years until he has that down payment.

Being able to buy a $200,000 house in the town I live in would change my life so much.

This won't change as long as property ownership and property renting is unified. There's just to much of a business incentive from renting, even if it takes decades to make it back. Worst that can happen is that it can sell it back to a market that criminalizes homelessness instead of treating it or its causes.

Keep in mind that 4 years ago was COVID times when everything was shit.

House prices exploded during Covid. Yeah, they dipped for like 2 weeks initially, but then they skyrocketed.

Not that this is "ok" but it's why "buy whatever you can as soon as you can" is good advice. If you'd put whatever you had into a shitty condo four years ago, and kept saving at the same rate, you'd likely be in good position to trade up soon.

I see a lot of people I know end up in the same position because they've been waiting for either the exact right circumstances or for prices to "crash." All the people i know who started with anything they could afford now have a huge amount of equity in nice homes. The difference is real and primarily about timing more than income or location.

I think you misunderstand. He didn't have the financial wherewithal to acquire a home of any sort because a down payment was expected even of the shitty condo. He didn't have the money then he doesn't have the money now he's on the same shitty treadmill that the rest of us in the permanent underclass are.

I bought 5 years ago when it was still reasonable. I have a great rate on a great house that has increased by about 50% since I bought it.

I don't want to, because this is just about the perfect size house for us in a great location, but I can't really "trade up" as the interest rates are through the roof and everything is more expensive too.

If your circumstances change, you can make a lateral move and invest the net profit in an index fund.

If it makes you feel any better, that house would sell for at least double that price where I live.

At least triple the price in my area. 4x if the schools are good.

So occasionally I look out of curiosity and the reason is pretty plain.

I look for houses for sale in a suburban area as public listings, and there's like 1 within a few square miles of the area.

I switch over to renting, and there's like 12 houses just like the one for sale available, all owned by companies. I also know a coule that aren't listed that have no tenants, but are still owned by one of those companies. You can tell because those yards are now waist deep grasses (in an area where HOA throws a hissy fit if your yard looks just a smidge unkempt).

Don't know why the companies find it more profitable to buy houses people aren't looking to actually move into, at least at the rent they are willing to accept. If I fully understood why, it might just piss me off more. Like maybe the houses work better as a loan basis than other assets, so even empty and unused they are valuable as some sort of financial trick.

Don’t know why the companies find it more profitable to buy houses people aren’t looking to actually move into, at least at the rent they are willing to accept. If I fully understood why, it might just piss me off more. Like maybe the houses work better as a loan basis than other assets, so even empty and unused they are valuable as some sort of financial trick.

That's one thing, but housing has been a low-risk investment for a long, long time. If they bought the house OP posted in 2020 and sold it in 2024 they would have almost doubled their money even without renting it out.

My understanding is that these companies are investment companies that need stable assets for their billions of dollars portfolios and they actively look to keep buying property as a stable form of appreciating asset. They have so much money that needs to find some way to make more money for their investors.

This is because venture capitalists are buying all the homes to rent

Said it before: no corporation except non-profits focusing on housing should own retail property.

About everywhere... In Toronto it's now 1 million+. In Vancouver it's now 2 millions+

Right but OP is talking about a house in Waleska, Georgia, which has a population of 921 (as of 2020 census). Not really on the same level as Toronto or Vancouver!

My janky duct tape together house I bought in 2010, that was built in '58 was 98k. In 12 years I sold it at 280k, with it still technically being out of code. My house was the cheapest sold in the neighborhood, some selling for 320k. It's insane.

Y'all realize this is a bubble, right? I almost feel sorry for these investors, gonna have their ass handed to them in the coming decade.

If Big Macs, houses, gas and college tuition all went up, it's time to realize these are not all in bubbles and instead realize due to inflation your salary has been halved.

No true! Plebs got 12% raises over last few years ans even for one quarter outpaced inflation 🤡

Y'all realize this is a bubble, right?

Can you explain why you feel that way?

Not really. The system will instead keep finding ways to get people to rent at higher prices or take out low down payment loans with ever larger monthly payments taking a lot more of take home salaries and making it harder than ever to save and invest.

The rental aspect isn't a bubble. Until they start viciously taxing single-family home rental, home prices are going to stay high because they're not being bought as homes but as assets for rent-seeking.

Shout out to [email protected]

It depends on the area. Some places are actually gowning that fast in population

It’s the same in Kansas City. I just checked a random house in my city and it’s up almost $100k in 4 years.

3bd, 1bath 976 sqft

Houses in my neighborhood are up 150-200%.

Didn't think I'd ever see Waleska on Lemmy... but, yeah. This is just the story all over North Georgia right? No one wanted to live in the mountains until all of the sudden you could work from anywhere. Now everyone earning city and suburb pay is happy to live an hour farther out than they were before.

Yep, that's on track! My house has almost tripled in price since I bought it 12 years ago. Denver metro. No way I could afford it if I had to buy it today.

Also here in Europe this is the type of construction we use for a garden shed, not a house.

Even when we do modern timber frame, it's generally still brick or block at the bottom. How long do these houses last in the US? I imagine a lot of the continent is pretty humid

It’s a good thing you aren’t a building engineer.

My parents' timber house is from the 1780s and is still solid. So, 240 years at least, give or take. I'm aware of plenty of timber houses from the 1600s that are still standing and functional as well.

Is a timber frame house from back then the same as one built post 1950 though? Some Q's:

- Have materials/practices decreased in quality?

- Has there been a shift from a sense of pride in craft and duty to build well towards cutting corners and saving $?

- Has the density and properties of wood changed as we use smaller trees grown more quickly in monocultures compared to old-growth harvested lumber of pre 1900s?

When wood is properly sealed up in walls, it lasts a very long time. We don't really have buildings on an old world timescale, but we do still have colonial wood frame buildings.

Timber frames are sheathed in treated plywood and then wrapped in siding. Rain doesn't reach the wood of a barely-maintained house, exterior humidity won't do damage in any hurry, and wood is rarely making ground contact. These houses last at least a hundred years given that this style is approaching 100 years. It's usually storm damage through the roof that causes the rotted wood you're imagining, not normal wear and tear.

In California at least, houses made with a wooden frame are usually on top of concrete (either a concrete slab under the whole house, or a concrete perimeter under the exterior walls), and the frame is bolted into the concrete along the entire perimeter.

Older homes often aren't bolted into the concrete, but it's common to retrofit this to improve earthquake resistance. Without the bolting, the house can move around during an earthquake. The government here has a program (Earthquake Brace and Bolt) where they cover part of the cost of doing this work.

Masonry (houses made of bricks, stone, etc) are much less common here, since they perform much worse in earthquakes.

👍 in Europe earthquakes luckily are less of a concern, so we care more about longevity (you'll find many places where pretty much every house is well over a hundred years old (the oldest one in my village is about 900 years old)) and good isolation (to keep the heat inside in winter and outside in summer so we can heat less / don't have to use air conditioning on our way to net zero)

In the lat 80s / early 90s, my SO and I saved up for 7 years to be able to afford the down payment for our first home. Now, that would be more like 20 years, which is too much.

Time to consider moving to Europe or Costa Rica or Mexico City or somewhere, if you're in that boat now.

It's not as bad in Germany, but pretty close. It's a very good time to sell houses. And on top of that they are generally much more expensive than American houses to begin with.

Literally thinking of going back to the old country. Least I could own a compound for that i pay for a caravan in a first world country. If only I liked sun....

Keep in mind that inflation has risen over 30% in just the last 4 years, which explains at least part of the rise in prices. I wouldn't be surprised if inflation is even higher in certain areas of the country. I'd also not be surprised if Georgia is getting a lot of natural disaster refugees from places like Florida.

The other part i don't see anyone mentioning is that this was all projected as a result of millennial generation, the largest % of population by generation comparison, came into the age of buying homes. Creating a sharp spike in demand over supply.

That's cheap as hell compared to California. And I work remote from anywhere I want. Thanks for the tip!

:laughs in Australian:

Are other homes increasing as much in that area? Or did they build a double garage, remodel the kitchen and install 15 swimming pools?

For my area it's all of them. Could have afforded a home a few years back. If you bought in 2014, 23000 got you a massive home with 4 car garage. Now that how is 600000.

House down the st was 94k in 2015, it sold for 195500 last year.

Bought our cottage for 50k at the peak of the rural movement in 2020 after it had been on the market for months, just sold it while the second property market has completely crashed for 130k after putting 10k in it and cleaning the fuck out of the lot (the place was disgusting, I'm talking 90 industrial garbage bags of crap, mostly beer bottles, a couple tons of wood and concrete and so on)...

Sometimes you're just lucky and people don't want to do what's required to get what their property is worth!

What I'm hearing is that houses have the ability to be a great investment.

Work to get a house and then when you are old and ready to retire you sell and then have a great retirement.

mine is now worth 130% of its original value

Has the population jumped up for ya guys?

Don't know about them specifically, but it seems that more than anything real estate investors are just grabbing as many properties as they can find, whether they can get tenants or not. A house goes up for sale and it's bought sight unseen by a company almost instantly.

That’s crazy

Yes the largest generational share of the population is the millennials most of whom are just becoming the age of the average first time homebuyer. Creating a sharp spike in demand for realestate.

Ya but does that happen with every generation then? Having a sharp spike of first time homebuyers.

Most millennials would be buying homes already. The end of the millennial group is coming up on 30 so I wouldn’t expect them to be the driving force for first time buyers when so many are already established

In my area, it's a 100-150% increase in four years.

It doesn't sound like much until you see numbers.

A $350k house is now $700k for no reason.

A $400k house is now a million.

It's depressing.

You want to know why? Start at the bottom and look at the price of land only blocks in the region. More than likely: its the cause. The answer then becomes very simple.

$325k for a 3bdrm 2bath detached SFH in good condition?

Awww, that’s adorable. Even after taking the exchange rate into account, that would be like going back to 1998 in my corner of Canada. Right now, a house like that on a 0.21 Ac plot of land would be running you $1,300,000 CAD. In places like Vancouver? $4,800,000 CAD on average.

Awww, that’s adorable.

People still talk like this? Wow. Anyway, it's not a contest. Both scenarios can be very unfortunate and disappointing

Real talk, forget about a down payment. There are a bunch of different ways to get a 0 down mortgage with varying qualifiers so that chances you qualify for one of them is quite decent.

Even if not, there are still a bunch of other ways to get low down payment mortgages for ~3% down or less.

Toss out the old adage of "20% down or bust" and keep any money saved towards it for savings for all the other costs of home/closing

This is terrible advice. Paying anything you can up front saves you several times over in the long run.

Let's talk 500k house, 6%, 30 years, no pmi, no taxes, no extras...

Paying 100k (20%) up front you'll pay: $863,352.76

Paying 50k (10%) up front you'll pay: $971,271.85

Paying 0 up front you'll pay: $1,079,190.95Paying 20% down (100k) will save you over 200k.

If you intend to live in the house indefinitely, you're so much better off if you put as much into the down payment as you can.

Edit: List formatting

That's great, in theory. In reality, you'll get stuck in a perpetual savings cycle like OP and in many cases never reach the mythical threshold.

200k savings sounds nice, but if you have to spend 5 years saving and housing prices jump 80, 90, 200% in that time that savings lead gets entirely erased.

You can always play around with your interest rate later on, but you can never change what you paid for the house

Also pay on time and as much as you can. Don't fall into the trap of paying to close to or at the minimum. If you do that you will be in loads of dept.

The longer you wait to pay something off the more interest it gains.

This presumes you can elect to either just spend the 100k now, that you may not have.

If you declare you want 100k, but let's say that would take you 10 years (and the goalposts wil move). That's likely 120 months of rent you will have to pay, so while you'll end up saving on interest, you'll more than lose out on rent.

Paying down aggressively and going with as big a down payment as you can reasonably afford makes sense. However waiting to save up for that downpayment may cost more in rental expenses than you'd save.

This is terrible advice. Paying anything you can up front saves you several times over in the long run.

Usually, yes, but it's situational.

For example, I bought my house in 2009 during the depths of the Great Recession, with no down payment, and got a screaming deal. If I had decided to wait a few years to save up for a down payment, I would've been 500% screwed.

(That "500%" isn't hyperbole, by the way: that's how much more I would've had to spend to buy my house now instead of back then! Actually, I'd have been even more screwed than that, considering that I'd be paying ever-increasing rent the whole time, too.)

What income to loan ratio are you talking here?

Houses only increased a little bit. The rest is inflation making your salary 30% less

A little bit.... Bahaha Hahaha ya ok guy. Just a little bit

The answer is to go somewhere cheaper. If you go far enough out of town the prices will go down.

Plus when the town grows your property value will go up and up.

The answer is to go somewhere cheaper. If you go far enough out of town the prices will go down.

So basically, somewhere no one wants to live because of distasters, is boring AF, no jobs there.

I once lived in a town of around 1,000 people. It had everything I needed in walking distance - a grocery store, doctors office, pharmacy, post office, restaurant, bar, and mechanic. A beautiful bike trail and river ran through the town. Fiber Optic internet was available, and there was a medium-sized town 15 minutes away with good jobs.

I just checked and the average home price is still around 100k. A 2br apartment rents for $750/mo. These places still exist, but they're called hidden gems for a reason.

Yep, everyone who lives in the less populated areas is miserable and bored constantly. Those poor people, so sad. They should be more like you.

Kind of yes. However if you want home ownership at a reasonable cost that's the way to go. It doesn't need to be in the middle of no where but it doesn't need to be in the upper tier locations.

This is a boomer logic...

- You are going out so far out that commute arouns trip will start @ 2 hours

- Both people must have reliable vehicles, cost of whivh also spiked. Whats total cost for a reliable vehicle now?

Congrats, you are living a miserable life with mortgage, 2 car notes and commute that destroys your health.

Played yourself really.

Yes this thinking really underestimates the cost of driving and devalues your time.

And as you mentioned, long commutes are uniquely unhealthy.

If the house hasn't changed, then the value is basically the same.

The price change is more about how rapidly the USD is devaluing.

Between 2020 and 2024 there was about 22% inflation. 1.22x$195,400=$238,388. So there's still over $110,000 of price inflation to account for past devaluation of the dollar.

there was about 22% inflation

I'm not disagreeing with you, but I just wanted to note that inflation numbers (more specifically, the CPI) is an average across multiple industries - supermarkets, rent/mortgage, furniture, cars, flights, health care, and several more. It's possible for inflation to affect some industries much more than others and I wouldn't expect everything to all go up at the same rate.

Thank you for eviscerating him-, oops, I mean providing that additional insight

Work from home is the ultimate culprit.

A. People can migrate and buy in cheaper parts of the country and maintain jobs that would have required them to stay in a certain geographical area in the past.

B. Work from home has gutted the commercial real estate market. Leading investors to move into the home market. You’re going to see a lot of money flow into single family homes to rent over the next ten years.

You’re now competing against established professionals who are later on in the careers and institutional investors.

100% WFH jobs have rapidly dried up. They're not super common like they were in 2021-2022. Most places either went back to the office or require a hybrid setup (x # of days in office every so often). I won't deny WFH jobs have definitely contributed to a general rise in home prices in some areas, but I'd need to see data proving it is heavily contributing to a rise all over.

One of the missing pieces that was mentioned by someone else is the purchase of residential properties by businesses being at all time highs.

WFH is efficient and makes sense in many cases. Private equity firms buying homes and holding them to sweat out the market far beyond what a solo landlord could or would, does not.