How are you doing financially?

How are you doing financially?

I read that half of Americans couldn’t cover an unexpected $1,000 expense. This sounds crazy to me. I understand that poverty exists, but the idea that an adult with a job doesn’t even have that amount saved up seems really strange.

What’s your relationship or philosophy with money? What do you credit for your financial success, or alternatively, what do you blame for your failures?

For the extra brave ones: how much savings do you have, and what are you planning to do with them?

It comes down to if you rent.

If you have a fixed mortgage, shit gets easier fast. If you rent, any wage increases is often offset by rent increases.

Less people are able to save, because they never get out of those "tough first years" of a mortgage

Renting is such bullshit these days. The payments they ask for rivals mortgage payments from just 15 years ago.

Less than that, especially in areas that used to be cheap.

It took less than 5 years for my decent sized house on almost an acre in a middle sized city to be less than a 2/2 apartment.

It's fucking insane.

I have rent control. Buying is the worse financial choice for me.

Idk it's pricy to own a home nowadays unfortunately. I bought only last year and my mortgage payments are a bit higher per month than people seem to pay for rent on a similar type of unit. It's not that I got a "bad deal" on the residence either. Home prices just don't make sense nowadays.

I will say that around 2931, rent prices in my area skyrocketed up a whopping $400-600 in one year, but they have since seemed to stabilize.

While your fixed rate mortgage costs don't go up every year, your property taxes, insurance, and HOA fees will. So with the above in mind, it doesn't really seem as economical anymore to own a home.

School and medical debt as well... The more you make, the more they take... Always keeping you at barely scraping by

Live below my means, invest the rest.

I don't dress or act like people in my pay range. My house is small and in a quiet neighborhood and cost less than my salary. Car is older but paid off and I know all the quirks and have the toolbox in the back to fix it. It is probably one of the top 5 most reliable cars in history. My work dress shoes are 10 years old and my around the house shoes were new in 2019.

I spend my money where I spend my time. So I have a nice phone, a very nice monitor and mechanical keyboard, and a good computer. And all with the right to repair philosophy. Same for my wife and kids. And also good running shoes, good exercise equipment.

The plan is to get to a point where I can just not work at all and maintain my lifestyle. Three percent rule and all that. And also help launch my kids.

Something about a 25 year roof and a Japanese shit box car in my fortress of solitude.

FWIW I grew up really really really poor like you wouldn't believe so I'm okay with this.

I grew up upper-middle class and have largely the same philosophy. Always thought my friends’ parents were idiots for buying these gas guzzling Ford/Chevy monstrosities just to haul around 1-2 kids and a dog on occasion. Regular salaried people spending/financing more than half their annual income every few years on cars they don’t need just to keep up with the Joneses who don’t really care in the first place.

I don’t skimp on quality when I buy something, but I only buy what I actually need and if something serves its purpose, I hold onto it for as long as it works. My wife and I do very well now, but aside from living in a fairly nice neighborhood with great public schools and amenities, you wouldn’t think it from the cars we drive and the way we dress.

I just don't understand it. I see some people with $1000 car payments and nothing toward retirement. What ever happened to looking for good deals? We had a kind of "rugged ingenuity" thing growing up where you respected people who took care of their older stuff, and I guess that still holds true today. $1000 car payments, I would have paid off my car in under a year.

Honestly, I'm scared to spend. Which I guess is okay because I'm comfortable with how we live and sometimes you have to spend on life events out of your control.

So I have a nice phone, a very nice monitor and mechanical keyboard, and a good computer. And all with the right to repair philosophy. Same for my wife and kids.

Jeez man, I'm happy for you, but most of us are stuck with stock model bullshit that broke in 2016. Go brag about your consumer friendly right-to-repair family in c/BuyItForLife.

(I kid, of course 😊 Solid approach you have there, smart and sustainable)

Yeah, thanks. Between ThinkPads and system76 and Fairphone, it's pretty easy to maintain. Monitor is a Dell U3014. It was over a thousand dollars new but these days it's under $200 used and I've replaced the mainboard in it twice for about $145 each time. Everything was purchased slightly used so that saves a lot.

All of this is great except the shoes, get some new/better shoes it's worth it, your body will thank you later.

top 5 most reliable cars in history.

i'm listening. is it an old corolla?

Camry

I'm with you on most of this but I think having a reliable car is pretty important in the US due to lack of good public transport. In many cases, after a car gets to be a certain age you end up having to repair too many things on it and it becomes an unreliable money pit. I'm very glad that hasn't happened to you, but I think for a lot of people it makes sense to get rid of their car once it gets too old. And then try to buy a lightly used car outright.

I kind of don't really drive much. Between biking and living close to a lot of things, I've put about 40,000 miles on the car in 7 years. Car is in its third decade and has about 70k miles on it.

This is essentially my situation too. I spend quite a bit of money on these small purchases for hobbies. But I'm easily clearing a couple hundred a month to buy stocks, save, do something really stupid, et cetera.

What’s your relationship or philosophy with money?

A life-changing shift to my approach has been to worry about absolute amounts rather than percentages. Saving $10 on a $20 item feels great but ultimately is the same thing as saving $10 on a $500 item (which feels like nothing).

I grew up lower middle class: never had to worry about not having a roof over my head, but there were times we were somewhat food insecure, and spending money on leisure/entertainment or anything unnecessary for survival was a foreign concept until I got to high school and some my parents' career moves paid off and put us in upper middle class. It took them a good 10+ years before they could relax a little bit and feel secure with their money, though, and that was as much driven by the fact that their kids were adults who had moved out.

So life has been about deciding which of my parents' frugal attitudes and approaches to money to keep and which to discard.

Things I decided not to adopt:

- I slowly learned to stop caring as much about wasted food. Food is just cheaper now compared to when I was growing up (even if the last 5 years has shown an uptick), and as a society we have more issues with obesity than hunger, so cleaning off a plate seems like it doesn't actually do that much good.

- My time is worth something to me. I will gladly pay the few dollars here and there for convenience.

- I'm glad I ignored my parents advice to buy a home as soon as I could and build equity or whatever. I rented and it worked out great for me, giving me the flexibility to make changes at different stages of my life.

Things I kept:

- Life is uncertain. Always be prepared with whatever you can accumulate for financial resilience: cash, other property, lines of credit, marketable job skills, literal insurance policies, etc. Don't underestimate the importance of personal relationships, whether it's "credit" from friends and family who can help you out of a bind, colleagues who can refer work to you, bosses who will fight for your career, etc.

- Develop your career. Education and credentials are important early on, and up-to-date skills and a good understanding of the landscape in your field (both in the type of job and the type of industry you work in), plus solid relationships with people, can help you know when switching jobs is right for you.

Things I had to learn on my own:

- Life is unfair. Many types of unfairness are systematic. So why not position yourself to where the unfairness works in your favor, if available?

- Higher income makes it easier to survive mistakes on the spending side. To flip around Ben Franklin's quote, a penny earned is a penny saved.

- Know yourself and your own laziness. Set up automatic functions wherever possible: automatic bill pay, automatic savings, automatic investments, etc. Steer away from any strategy that requires active management, and towards strategies that tend towards a set it and forget it philosophy.

I've also made a shitload of mistakes, some of them pretty costly, especially back in my 20's:

- Paid probably thousands in credit card interest in my early 20's chasing lifestyle bullshit.

- Paid thousands in unnecessary car loan interest in my mid 20's by getting suckered by a dealer.

- Paid hundreds, maybe thousands, in late fees and interest from forgetting deadlines to pay shit I actually already had the money on hand for.

I'm rich now, most of it from luck (especially timing), much of it from personal relationships (good family, good marriage, good friends), some of it from actual effort (good grades from a good law school), and some of it from conscious decisions to steer towards my strengths and away from my weaknesses (lazy but smart, prototypical "gifted" slacker with undiagnosed ADHD).

It took a while to get here, though, and I was financially insecure well into my 30's. Sorta figured shit out then, and then married someone who complements me pretty well on these things, and covers my blind spots.

For the extra brave ones: how much savings do you have, and what are you planning to do with them?

I have some savings, and it's an emergency fund. It's representing 1-2 months of typical spending, that could be stretched to 3-4 months if I needed to stop the frivolous spending. But I have credit beyond that, and less liquid assets I'd be able to tap into if I were facing a longer term issue.

But I'm not saving for any particular thing other than retirement. If things accumulate and grow, great. I'll make a judgment call on when to retire based on how I feel and how much I have and what I want to do. I anticipate my wife and I will probably want to retire in our early 60's, based on our anticipated career trajectories and the ages of our children.

Really interesting read. Thanks for the response.

Why do you only have a few months' worth of savings despite considering yourself rich? Or are you just speaking about cash reserves?

Or are you just speaking about cash reserves?

Yes. Cash reserves are like unused RAM to me: I have it, so I might as well put it to work. If it turns out I need it somewhere else, I can always go rearrange things to make that possible.

Realistically, I think I'm rich because my wife and I both have strong ability to command high salaries, switch jobs, etc., even in a pretty severe downturn. The main things that might tank the value of that expected future cash flow are disability or death, and we at least insure against those.

We also only need one of our two incomes to support our lifestyle, so we have a certain resilience that just comes from having that buffer. At our current ages, we also already have substantial retirement savings, so we have some resilience there, too.

The but about higher income making it easier to have mistakes is a big one.

I have a friend online who wants to make money, but doesn't seem to have the ability to do so without going back to school. Going back to school would incur student loan debt, so they do not wish to do so.

I have a crazy amount of student loan debt, maybe $150k. But people don't understand that federal student loan debt is absolutely nothing like credit card debt. There are basically no downsides to it besides paying another monthly bill (that you can use an income based repayment plan for).

People don't understand how incredibly useful excess income is even if it ends up with a lot of loan debt. I had a similar hesitancy back before I went back to school, but I don't regret it at all. I think I ended up like tripling my income.

Even if you end up with a lot of loans, making say $80k/yr is astronomically easier to survive on than $40k/yr for example. You have to think that something like rent or food prices are going to be somewhat similar in your area no matter how much you make. Sure, you could choose to live in a lavish place I suppose, but if you live reasonably then it's more than worth it.

As an example, the average rent price for a not shitty one bedroom apartment in my area is maybe around $1.6k, which would equate to $19.2k/yr. That's almost 50% of the gross income of the person making $40k/yr while only around 25% of the person making $80k/yr. So even if the person making $80k/yr has a $1k/mo student loan bill (you can get it cheaper if you wish), the difference is dramatic.

The person making $40k/yr will have a little over $20k left over at the end of the year for remaining expenses and savings, but the person making $80k/yr will have more than double that at $48k left over. Obviously there are a lot of nuances in this but still.

So it's absolutely worth it to incur federal student loan debt if it means you will make a lot more more money. Private loan debt is a bit different.

Yeah, I'm not going to pretend like I'm good with money. I'm not. I have a decade of experience of being a young adult on a tight budget to know that's not one of my strengths. I wasn't great at stretching each dollar to its most efficient use. And I still am not.

I won't speak on whether student loans are worth it. I think, like everything, it depends. I think a bachelor's degree is definitely worth the cost (both in tuition and time), but it might still be worth doing it cheaper if there's a cheaper path available.

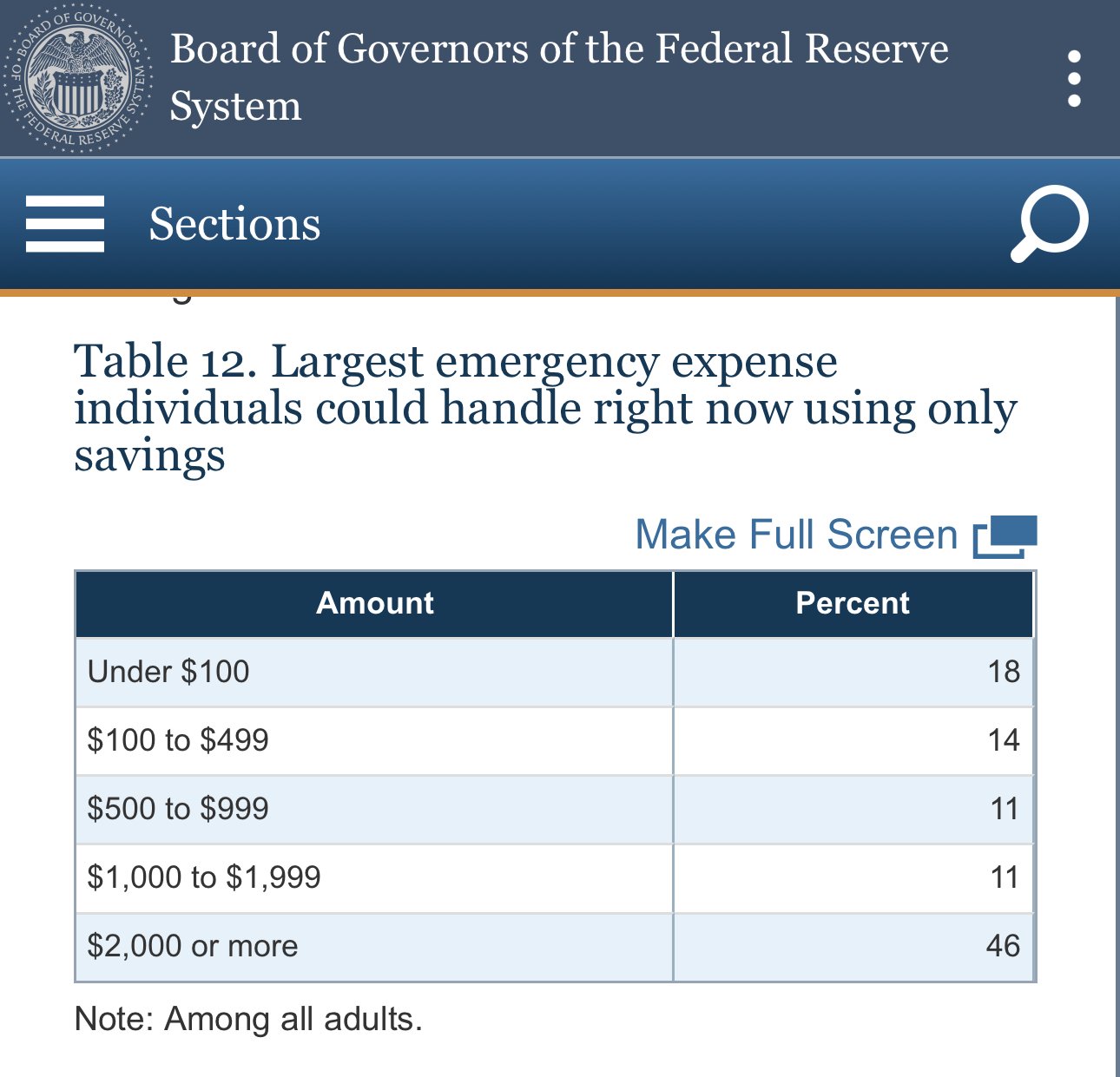

They release data for stuff like this. Currently 46% can cover a cost of $2K or more with just savings. 57% for $1K or more.

But it’s even worse than that - what kind of emergency is that cheap? Sure I could replace tires in my car within that amount, but could not repair a car accident. I could visit an ER within the amount but could not pay for medical care for sickness or injury. I could call a plumber within that amount, but not not repair or replace things after a leak. I could travel to see my elderly Mom if she were sick, but could not afford a place to stay there within that amount

every time I read one of those statistics, I feel the same way.

I'm doing very well relative to that statistic.

I live fairly simply, but I don't consider myself particularly frugal.

I like traveling, learning, eating, watching and reading stuff, and making things, which are all pretty cheap interests.

If I were to credit anything with my financial success, it would be a practiced awareness of financial opportunity and persistently learning about and attempting every viable opportunity I'm interested in to gain a practical knowledge of cost-benefit streams.

I've tried many ways to make money and work less, and some of them worked out.

I'm traveling this year, so I save most of my income, and with the IRS' FEIE I don't pay income tax(up to 120k).

I have a few investments and some ten thousands accruing interest.

i don't have immediate plans, but I want to buy some land at some point, basically so I have more area to build stuff and make stuff, sign up for cryonics and get a new electric bike or the Aptera if it every goes into production.

c'mon aptera.

It’s a difficult subject to discuss without sounding like you’re either bragging or talking down to those less well off.

I recently bought a new-to-me truck. I paid in cash, and if I wanted to, I could’ve bought two more. If I liquidated my investments, I could have bought three more, so six in total. I’m self-employed now, but I built all my wealth while working for a (plumbing) company where I was surrounded by people earning twice as much as I did. Yet, these are the people who need to finance their cars, have massive mortgages, and are always in a bad mood due to stress.

I understand that some people have been really unlucky and struggle to improve their financial position despite their best efforts, but these aren’t the people I’m talking about when I wonder how a working-age person can’t come up with a thousand bucks for an unexpected expense. I hardly even consider that a lot of money.

but I want to buy some land at some point, basically so I have more area to build stuff and make stuff.

I feel you there. What kind of things would you like to build? For me, it’s things like a rainwater harvesting system, solar/wind power, a pond with a pier and sauna, a chicken coop, a heated workshop with a car lift, a root cellar... I basically have an infinite list of projects I'd like to pursue.

"I basically have an infinite list of projects I'd like to pursue."

this is about where I'm at.

All the homesteading stuff, I want to try breeding meat rabbits, I want to try geothermal air conditioning, buy used cars and flip them (I started working on cars a few years ago and ended up enjoying it much more than I thought I would).

a whole separate area for home brewing and jerkying stuff too, canning, all that.

I like the idea of building different types of housing and read books and watch videos all the time, like straw bale or clay or underground, whatever the heck experimental cabins I could build, and I've further toyed with the beginning of an idea of how to turn that into low income housing after I land on the simplest, sturdiest and least resource intensive houses to build.

carpentry. I've built small tables and desks and chairs for classrooms, but I'd like to experiment with larger furniture.

I did a lot of solar power experimentation when I was living in a motorhome that turned out Great, and I expect many of my projects outside would be solar and wind powered.

fish farming, vermicomposting, yeah, just a thousand billion things haha.

I like making things, building things, and new experiences.

I've done smaller projects within most of the fields I've mentioned as the opportunity arose, but even when I'm renting a house somewhere for a couple months I can't easily conduct long-term larger living experiments, so I'll have to get a house and land at some point so I can fiddle at scale.

..."always in a bad mood due to stress."

circumstance and opportunity.

some people don't have the opportunities, many do have the opportunities but don't recognize them or choose not to take them because anything outside of what they already know makes them uncomfortable where is seen as difficult, and they haven't been taught or learned themselves through experience to push past that discomfort or initial effort.

I have $15k liquid savings and another $50k I could pull from my Roth IRA in a dire emergency. It's not as much as I'd like, but I'd be ok if I lost my job. I live in a HCOL area so it doesn't last as long as you'd think.

I make a good wage, but I work my ass off for it. I credit my financial success largely to luck, my work ethic, and the great state of California. 10 years ago I was making $20k a year, now it's close to $200k. The main difference was I moved to California. No college degree, blue collar job. Skilled labor. I took jobs with companies that would train me, took promotions, and job hopped a lot.

I pay a ton of taxes and I'm happy to. I'm giving back to the community that enabled my success. If anything, I should be paying more taxes. I do donate about $80 a month to various causes, mostly carbon capture to eliminate my personal carbon footprint, because the environment is very important to me and I like to feel I'm not part of the problem.

I still have $20k in debt, on credit cards but at a promo 2% interest. I hope to pay it off in 2 years.

My philosophy with money is honesty not very healthy in some respects. I've been chasing dollars for years, to the complete atrophy of my social life. I've been pouring money into my retirement and have about $300k saved up in 401ks and IRAs. I also send a ton of money to my parents who are still stuck in the poor Southern state I grew up in.

In my next phase of my career I hope to transition to a job that will keep the same wage but give me a better work/life balance. I work 60 hours a week, add commute time and it's 75 hours a week.

I'm also fucking sick of working with all dudes. The trades are overwhelmingly male. I can go weeks without even talking to a woman.

I'm in my mid 30s. I came to California homeless in a beat up '92 coupe with $30 in my pocket. I'm the poster child for pulling yourself up by your bootstraps, so listen to me when I say I would not be where I am without the support of a pro-worker government and a huge dose of luck. Taxes are good. Unions are good. Worker protections are good. Even with all that, I am an outlier. We (the fortunate) need to do more to help others.

Wow, you make $200k/yr and only have $15k in savings? Not that $15k is a bad amount to have for the average person, but it just sounds so unbelievably low for your very high income. I mean, I knew the cost of living in California was wild but I didn't realize it was that out of control.

I only made $160k last year, this is my first $200k year. About $120k the year before. And I spent $18k on replacing my moms sewer system this year after hers failed.

It's a balancing act. I'm sending about $60k to mine and my parents' retirement accounts. Most people would recommend padding out my emergency fund before that, but I play things with a bit more risk.

But also yes, cost of living. Box of cereal, $8. Even if you're frugal, it's a lot.

I have $15.

Not just that I can spend. Not "until sometime in the future." Just $15.

feel ya. i had $8 left before my last payday and I'm guessing it'll be like that before my next payday too.

Im doing pretty well. Living in Germany, educated parents. Did okay in school, never studied much though. Went to university, got my Masters in Mathematics (needed to study a lot for that, but its my passion anyway). Started working at an IT company in the same city.

3 years later, I have around 50k in savings now. We live in a small apartment, are in the middle of buying a house.

Capitalism is really fckd up, especially in the US. I try not to take advantage of it too much, up my monthly donations with every raise, vote left-ish, dont support big corporations.

I think the biggest factor for success is luck for being born under the right circumstances. Thats like 99%, the rest is having some self control.

I’m doing well at the moment. The problem is that no matter how well I do, eventually something destroys my savings and eventually there’s a layoff at my company.

Even if I’m doing well at the moment, I’m still a couple paychecks from not doing well, and am no where near on track to eventually be able to retire

I have five digits of savings for the first time since my kids were born, but I also have college expenses for them, and at least that much in deferred house maintenance

I credit Apple, of all things. I always chose credit cards to minimize interest and fees, so this is the first time I’ve had one with significant cash back. Now I pay essentially everything with Apple credit card, pay off at the end of the month, get a surprising amount of cash back, directly into the high yield savings account. While of course my job is the reason I’m doing well, I credit this for turning things around to actually let me put money aside, to boost my savings

I am one broken leg away from being homeless and losing everything, and it's been like that my entire working life. I've never been able to make enough to actually save. Currently I have -100 in the bank and some debt I'm trying to pay off on top of that. My rent is literally half my income.

Went from living paycheck to paycheck to having a full $1k in my account right now after dumping my ex and moving out. I always thought that having two incomes combined would be better than just my own, but never realized how massive a drain my ex was compared to just taking care of myself.

That being said, I'm able to live cheaply because I use public transit, cook all my own meals, and I don't eat that much. I think for most adults in the U.S., especially those who need a car for transit, the honest truth is that their wages just barely cover all their necessary living expenses.

I've got $0.85 in savings, because I put my rent and car payment money in my savings account each month until I need to pay those bills. I did at one point have $1000 saved up as a rainy day fun, but then it rained for a whole year (financially speaking). Now I don't even have credit cards to fall back on, as those have been maxed out and gone to collections. I'm looking for a job in an industry I left because it was driving me to alcoholism (software), but that job market sucks a little more than the service industry, so I'm not optimistic.

Oh yeah and I'd be homeless if I didn't have family who were willing and able to loan me rent money.

I currently work on software in automotive. Everything seems completely insane. We have tons of process and technical debt, executives that are super out of touch and all have their own pet projects, we have hundreds of executives so we have 100 number one priority pet projects, we have a very distributed hardware/software footprint due to the affirmationed process/technical debt, each vehicle has a different hardware footprint which means we constantly have to make our distributed software work when a piece of the software needs to be rebuilt in a new controller, etc etc.

There's also the whole mess of trying to run agile at scale, managinga very distributed backlog, trying to balance priorities across teams that have to coordinate work, everyone leading with "how they want it" instead of "what they want", total disregard for WIP limits, etc.

I know where I work is a shit show. I really wonder if it's much better elsewhere. I also wonder if this place has always been a shit show and I just have more exposure to it now.

And yeah, alcohol. I'm trying to cut back but the mood here seems to violently oscillate between "this is OK" to "what the hell" and back again. We're probably due for another swing soon.

Some days I do think about going back to waiting tables. It took me years of working elsewhere to stop having the waiting weeds dreams though...

I'm digging myself out of a $13k credit card debt hole. I burned through my savings when a job that I had ended on my unexpectedly, and because it was contract work I wouldn't qualify for benefits. They kept me around as a sub, promising me a full time position if I just stuck around long enough and I was foolish enough to believe them.

I'm self employed now and making do with the best I can, but I'm planning on ending my dream as a musician/ teacher and moving home. I don't know who would want my skills, but I know they are specialized and strong. I just gotta see what kind of work would value them.

I have a decent amount of money in a 401K that I can't touch, and some stocks I bought during a time when I fell into a bunch of money, but an unexpected $1000 would not be possible. I'm a 42 year old married man with 5 kids and a full time job at a small college.

I should be doing better than this.

With 5 kids, I'd say you're doing alright. Kids are so damn expensive.

Yeah being able to afford 5 kids is insane to me.

Im doing well. Started off in my mid twenties reading books on finance and investing. Lived in a drug house where I rented out a room and had a dead end job. Got an education, decent job, and invested aggressively for the next 20 years. Im planning on retiring in my mid 50's if everything goes to plan. 🤞

I was born at an unfortunate time. By the time I could afford a house the housing market was already very bad. I'm just glad I'm able to buy a house but it is very expensive (we bought at the end of 2021)

I live in Canada so we can't lock in our mortgage for more than 5 years. I just went with the variable rate because in the long term it's generally better. However the interest rates skyrocketed. I was able to pay my mortgage still but I was pretty much house poor.

Now the rates are finally dropping so I feel a lot less pressure. With our current budget we should be able to afford one kid comfortably. I'm not sure about a second.

I'm very fortunate and grateful though. Most people my generation cannot even afford a house. It's just insane that despite my great job it's still so hard for us I can't imagine what others are going through.

We aren't broke. I have some retirement saved but I had to stop putting money in due to our mortgage. I also have an emergency funds account with enough money to sustain us ~6 months if I were to lose my job.

Having a high paying job is unsurprisingly the main reason for my financial success. Otherwise I'd say joining some personal finance clubs helped a bunch. I have my savings diversified and invested so I'm at least not losing money to inflation. But my investments will never make me rich either.

One critique I have for myself is maybe we overspent on the house but at the same time I love our neighborhood and I love our house and we have no plans on ever moving so I'm not too upset by it.

Since I left college and started out into the "adult world", I've always spent less than I made, the rest going to savings or investments toward retirement. I accomplish this by "paying myself first". If I have already saved the money as my first priority, I can't spend it on things like rent or groceries. So my financial choices are forced to be more conservative by design.

Example: I forget what the max limit to IRAs were at the time (say $5k/yr) but for my first job I set up auto contributions each month and mentally took a $5k/yr salary "cut" for that job. Every time I got a raise, I made sure that at least a portion of that raise went to increasing my savings rate and attempted to avoid lifestyle creep.

Thanks to my savings, I've been able to handle some emergencies in cash vs having to utilize debt to cover the expenses. It really is a snowball. I started out small, now my savings is significant compared to my income.

I attribute a lot of my "pay yourself first" approach to reading The Automatic Millionaire, Expanded and Updated: A Powerful One-Step Plan to Live and Finish Rich early on.

I'm doing well but i wish i could afford my hobbies.

I dislike money. I worked hard to have enough that it’s not on my mind. I don’t need to think about the cost of eating out or buying food, or pursuing hobbies. But I also don’t really spend much. I don’t make big purchases very often and when I do I still over-analyze them.

If I had a lot more money I could retire, but I still have half my life to live. I hope to retire in 16 years. I have a job that pays well, with good job security, and minimal stress. I get 38 hours of leave time per month and I live in California.

I have cash savings earning enough per month in interest to pay my cell phone and home internet bills entirely. But I don’t really have any other discretionary monthly subscriptions. My savings will probably be used on a new kitchen and bathroom eventually.

A 200k expense won't destroy me or lock me out of my house or completely destroy my retirement. No inheritance, went to college, and knew buying a house early was key, saved about 25% income for 3 years to put 45k down on house.

I'm doing well, but the job is sucking my will to live, and I think about quitting and going to work in a bakery or farm every day

I have always strived to keep between 1-2 month’s worth of expenses in savings at all times. That small buffer has allowed me to ride out almost everything without going into debt, then when I am in debt I pay it off as quick as possible.

The worst thing you can do is get on a payment plan, as that normalizes having debt and you end up paying thousands in interest. All interest is, is you giving your money to someone else. I like to keep my money, so if I have to live off of ramen and hot dogs for a couple months, so be it.

All my jobs have been paycheck-to-paycheck until about 3 years ago. My last job allowed me to save up $24k, but then I lost my job. Now I'm down to $7k and getting worried.

I know the feels, you are not alone

I have a job. It's technical, requires a fair amount of skills and abilities, yet I cannot cover a $200 emergency after bills and rent. Rent has jumped from $600 a month to $950 in less than four years, and the internet I need for my job has doubled in two years. Of the rent increases? Most of them were in the past year.

I am not American, but Austrian. I earn way more money than I spend each month, causing my bank balance to rise over time; I am not going to say exactly how much I have, but €1000 (which is about the same as $1000) is no problem for me to afford when I need it.

While it's better than the alternative, it still doesn't make me very happy because this only helps fulfill the bottom two levels of Maslow's hierarchy of needs. I wish I could easily earn less money, but have more free time to travel and pursue hobbies, but the system of wage labor is not flexible enough to cover the needs of someone like me.

Doesn't Austria have a law that allows employees to reduce hours to part-time as they see fit? We do here in Germany. Last place I worked at, my team lead didn't want me to reduce from full-time to 80%. The Betriebsrat (employee council) was ready to go to bat for me, but I didn't like the role anyway, so I interviewed for another place. They offered me 80%, a pay raise, a better role and benefits.

This might come off as bragging, I realize. Sorry, not my intention. I just wanted to share my experience, maybe it's useful to someone 😊

I can lose my job for a year and be ok. I'd probably cut back on some expenses, but it would probably be ok.

Great job! How did you get to where you are?

First, I chose a college degree that would lead to a career which would pay well out of college. I picked a more expensive college than I should have, but it was worth it and they gave me some scholarships.

Second, I lived under my means for the first few years. I made it a goal to build up at least three months' salary as backup in savings. I've rented, but only in places with rent control, so my rent doesn't increase drastically per year.

Third, after having a growing nest egg, I starting putting money towards my non-federal student debt to get rid of that payment, especially when I was working additional hours at work. I was able to pay off my 30 year loans in 10 years. After I paid that off, all the money I used for student debt went into my 401(k) and other investments.

I have enough in my emergency fund that if I lost my job I'd be ok for about a year.

I'm nearly to my goal, after that I'm going to change my focus to expanding my portfolio.

Still no way I can buy a house though. Need to make about 3x more money for that to happen.

I credit it to having a property owner that's kept rent cheap and having low overhead, and being frugal borderline cheap.

I fall between the government won't give me SSI because I'm not disabled enough in there fucking eyes. And being disabled and can't work.

So financially I'm fucked and nothing I can do about it.

Even if I had said It would only be iirc around 800 a month.

It's part of Amerikkka hidden eugenic programs. (Not verified but living with a disability it sure fuckin feels like it)

The last year has been rough on my savings. The retirement savings are untouched but the general savings have been emptied by a combination of travelling for family weddings and a downturn at work. I'm not worried but I do need to make a change.

Not saying the exact number, but well enough that I could go and buy an X5 right now. I'd rather spend any excess money on charities over materialistic status symbols though, and I've donated a lot of money to research charities in particular.

Hopefully you're also contributing to higher yield and tax advantaged accounts!

Maybe it helps to understand it when you think of it from the perspective that those $1000 expenses do happen, they're not just hypothetical. But being able to cope with an event like that leaves you less able to handle a second one, and a third one

Couple that with the fact that I'm the US there is very little financial education so what might be an expected event for one person surprises another. Imagine living with a roommate and not realizing that to move into your own place involves coming up with first and last month rent, deposit, hook up fees, renters insurance, furniture, kitchen supplies, toiletries, etc... None of those should be unexpected, but also why would you expect them if you didn't happen to run into them before?

Basically no amount of saving accounts for an expense that takes it all, and it's then followed up by another one right after. And for some people those events are small and happen so quickly you never catch up and now you have late fees and interest and stress.

Am early in my career. no debts out of college due to lots of scholarships and a bit of hwlp from my grandparents helped a lot. Bought a house, have a wife in grad school so pretty much just living off of one paycheck. Had to cover a 10k roof replacement last year which sucked, but am back up to about 25k saved up should I lose my job or face another major expense.

I am pretty frugal in general but spend money on a hobby every once in a while. Not into drinking or any legal or illegal drugs so that has peobably saved me thousands of dollars too at this point.

I was right on the edge of being able to pay rent on time, for the first time in six months.

Then a family member arrived in town and has been staying with me. His other option is staying on the street or in a shelter, both options of which make his health issues worse. This has disrupted my sleep and psychological rest, resulting in me being able to work less.

Also, I got rear ended while stopped at a red light last week, giving me a concussion. This has also reduced the amount I can work.

I’m extremely worried about my financial status. I cannot cover the expenses I have, let alone any unexpected new expenses.

I’m squarely on the road to being homeless, unless a miracle happens.

Ever read Miller's Death of a Salesman? well it's almost like that, but without any insurance.

I've certainly been worse of, but not I'm not.. Great. ButI have a roof over my head and me and the cat are fed. I can enjoy a video game here and there. However, I don't have $1,000. Not for lack of trying, but things happen (moved, sick cat, broken car, the usual). I personally like to have at least one month of rent, but that doesn't always happen.

Sometimes it just works out that everything I need takes everything I have.

I read that half of Americans couldn’t cover an unexpected $1,000 expense.

Without borrowing or selling property, yeah. Not a lot of people have that much liquid cash laying around.

But I wouldn't assume that this would be some kind of economic devastation. Our whole system revolves around easy credit.

If the unexpected expense is something that can be paid for on a credit card, that 20% interest isn't exactly ideal but for many people it can be a simple task of buying now and paying it off over 2 or 3 months. For them, $1000 isn't a lifestyle changing expense.

For others, $1000 might be devastating. It might be the difference between making rent or not, and ultimately lead to eviction and maybe even homelessness.

So liquidity is a different question from financial health or resilience, even if they're somewhat correlated. There are other metrics out there more directly measuring financial stability or vulnerability.

I credit my success to some hard work but mostly luck. At the end of the day my first job was from a recommendation. I believe interviewed well, sure, but I don't think they would've taken my resume otherwise. I'm extremely fortunate to be where I am financially.

Shit still happens though. I lost my job about a year ago and was unemployed for like 6ish months. I had enough money in savings that it didn't really matter but it still sucked. One thing that has been difficult for me is watching what I say. As an example, some stupid shit happened and I feel like a company owes us ~$800 and another one ~$200. (Not going into details because they're irrelevant and I want to move on from the stress.) These things royally pissed me off. I still get upset when little things happen and I lose money. I hate it. It sucks. As much as I want to get comfort from my friends by venting about it, sometimes it's better to shut up. Because some of them mostly just hear how I'm able to withstand losses like that and that in turn makes them feel upset that they aren't. It's a tricky thing.

As for my philosophy, for the most part my wife and I have been able to spend within our means without much aggressive or intentional budgeting. It's only been since the job loss and her being unemployed to pursue writing a novel that things have gotten tight. (And by right I just mean our savings aren't noticably increasing.)

Failures? Well, let's ignore stuff like crypto and stock picks because that's just gambling. I wish I had started maxing out my 401k in my 20s. I started on my early 30s. Also, we used to have a truly stupid amount of money in a checking account. We should've put it into stocks (as in total market ETFs) earlier.

OH. THIS IS IMPORTANT. I WISH SOMEONE WOULD'VE TOLD ME HIGH YIELD CHECKING ACCOUNTS EXIST. Like, holy hell. I should've done that ages ago. I don't even wanna think about how much money I've lost on, especially because we kept a stupidly high amount of cash in our checking account... I still haven't moved it because it's hard and I'm lazy but wow wow wow. This is stupidly important. The reason savings accounts are annoying so because it's a little harder to get to your cash. But a checking account with interest? Hot damn.

Lastly, I've never had a credit card. It's been fine but it would've been nice to get the tiny marginal benefits of cash back and stuff.

Financially, we are well enough to have my family’s needs met comfortably but frugally. Can’t really ask for more, though additional breathing room would be nice. We can afford emergencies and recover after some time.

My parents and grandparents taught frugality; luck made ends meet like a good job and buying a house at the right time.

We have a bit of savings I have in mutual funds because I’m currently too mentally tired and risk-averse to pick something with higher return potential.

There are a lot of very poor people in the US compared to other developed countries. There are also a lot more extremely rich people. The inequality is palpable, and it shows in the stats. The US government also doesn't step in with coverage when it comes to healthcare, unemployment and other emergencies to the same degree as governments in other western countries.

I can't cover an unexpected 1k. Thats my entire bank account. Every month my paycheck is eaten by bills and obligations and every other month my rent raises while my salary stays the same. I have 1 dollar in my savings, but a 401k with 5k in it. I also have kids and a wife that stays at home to watch them. May not be the best financially but I can't actually afford daycare to begin with.

Better than ever. But I hate my job with a deep and burning passion, and I'm pretty deeply burnt out. So I'm not sure what to do. I'm worried that I won't be able to find anything that pays as well.

Life's too short to stay in a job you hate. Collect some fuck you money from your earnings and move on. You wont regret it - even if it means taking a pay cut.

I can currently cover a $1000 expense, but if something else happens that costs that much I'll have to use my credit card, and if a third thing happens I'm fucked.

My relationship with money isn't good ("not wise" might be a better term), and now that I know my parents as an adult, I understand that both of them are terrible with money. Do I blame them? I try not to, but sometimes that's hard when I see how they continue to make poor $$ choices. My mom constantly made over 6 figures for a good portion of her later life, but now can't work, and she has nothing but social security to live off of. Through the years she's used up all her retirement and savings a few times on things like saving houses she eventually loses anyway.

My dad just dropped the news that he owes 80k to the IRS because he's been pulling from his retirement for years now to sustain his lifestyle in a high-cost area.

Myself? I didn't really get my shit together financially until I was in my mid 30s. Mostly my fault, though there were a few things that happened outside of my control that forced me to "start over" financially. That's life.

My relationship with money now is respectful. I take the time and care to slowly work my way through understanding what to do and how to do it. I only have one credit card and it's a low amount, so it can't get wildly out of control but it's there if I need it.

Right now I've got around 1.5k in savings (not including my 401/Roth). My plan is to save up to 10k for an emergency fund and then start to invest what I save up after that.

I listen to a lot of Caleb Hammer on YouTube. It helps, haha.

Same... Except my parents were teachers, so we were poor, because society is crap and doesn't pay teachers what they should be getting paid

My mom was a speech therapist in schools and my dad was an aerospace engineer. Theoretically they should have a very cushy retirement life. Nope.

I've always saved very aggressively, even when I didn't have any money. When I first moved out, I ate nothing but rice, lentils, eggs, and lard for several months to save a slush fund. Even today, I make ~15-20k USD below median income for my city, and I've managed to save just shy of 10k in the past year and a half.

Obviously the ongoing coat of living crisis is a big deal that needs to be addressed, but we also need to acknowledge that saving your money is unpleasant, and a significant number of people aren't willing to do what's necessary in order to build financial security.

My friends (I don't get out much, I only have a couple) all have significantly better income/expense ratios than I do, and have exactly nothing saved. Honestly I don't think that would change if you gave them all an extra $20k/year, because they will find a way to rationalize something into being a necessity.

My relationship with money is kinda weird. When I was a kid I would always save my allowance, but my siblings would steal it from me. My parents never did anything about it. When I had finally had enough, I stole some money back and then said all the bullshit excuses I had received over the years. The stealing stopped then.

I don't like money and I don't care much about material stuff. When I was in university, I was dirt poor, but I managed. Then I got a shitty job and didn't make a lot of money, but it was so much more than what I had before, that my bank account started to grow. And that made me very nervous. Every time I saw my balance I panicked. I didn't know what to do with all that money, there was nothing I really wanted or thought I could have. I did go on a vacation then, which was great, but I felt really guilty afterwards about the expenses I'd made.

After some time I lost my job and since then I've received benefits. Because of the system here and because I'm still quite frugal, I still have a significant back account. In a few months' time I will hear if I will keep receiving benefits or not, and if I spend the money now, it will be beneficial for me financially. I should basically buy something expensive and eat out and buy lots of clothes before the government takes my money, but I can't. I'm just not able to.

What doesn't help is that I hate the fact that the world is in such a miserable state. Sure, I could buy a car, but I don't need it and why would I mess up the environment even more just for my own pleasure and comfort? The same goes for clothing, equipment, furniture, anything. I don't like this capitalist system that produces crap and ruins the planet. I don't want it. But there's nothing I can do about it other than what I already do. Also, most of the stuff you can buy nowadays is just plastic crap. I can't even find decent cotton socks anymore, it's all plastic. And it all breaks way too quickly, just so you have to buy new plastic crap again. Fuck that.

Purchase some carbon reduction.

https://climeworks.com/subscriptions

These guys have giant CCS machines. When you send them money (which they use to fund their operations), they calculate what share of carbon reductions you've funded and they give you a certificate for it. It is NOT a carbon offset. They pull carbon out of the air directly and bury it in the ground.

I made a few bad moves in my 20s because I had no basis of understanding when it came to money (parents are bad with money too and never taught me anything useful), have spent my 30s desperately treading water trying to get ahead, but it seems impossible with rent going through the roof, food going crazy, plus now I have medical debt on top of my school debt... my really big mistake was wanting to help people by becoming a social worker.

What pisses me off the most is that if you're a plumber you get to walk in and demand whatever price you feel like, but if you're someone who helps society, society gets to cram it up your ass and tell you to smile about it. Same goes for anyone who works for society: teachers, cops, firefighters, EMTs, social workers, librarians, nurses, etc... I don't get why we don't all just join together and let society fucking die until they agree to pay us what we're really worth.

Edit: to clarify, I'm not saying plumbers aren't helping society. I'm saying when inflation goes up, plumber's prices go up to match... If you're being paid by tax money, you don't get to do that. Nothing against plumbers, it was just an example.

Everyone is getting fucked in our capitalist nightmare, but if you work for Walmart, WALMART investors are fucking you over... If you work for any of those jobs I listed above, SOCIETY is fucking you over (yes, I get that at the end of the day it's still those Walmart investors fucking us over because the same 1% own everything and stop society from paying us what we're worth by refusing to pay their fair share of taxes)

What makes you think plumbers aren't helping society? Same goes for all trades...like damn.

"Society" doesn't pay plumbers... Like, you don't get your plumbing fixed and bill Medicaid you know? Individuals pay for their own plumbing, and plumbers get to set their own prices... The jobs I listed are most often paid by society as a whole, and society as a whole are screwing these professions over... Don't get me wrong, most workers are getting screwed, it's just different.

dont wanna pile on... but idk, man... next time you use a functional toilet, you might want to consider what you just said.

plumbers are likely in the top 5 of all time life savers on this planet. just sayin'.

respect you social work immensely, but everyone's contributions are undervalued in this world.

What pisses me off the most is that if you’re a plumber you get to walk in and demand whatever price you feel like

As a plumber I can assure you that this is not how it works. I charge 60€ / h which may seem high but that's not what I pocket from it.

YOU charge... I don't get to charge for my services... I just have to take whatever society offers... In fact, with a lot of those jobs I listed, they are legally not allowed to stop working (strike) to get better wages BECAUSE it would fuck society so bad. I'm also in the US, so my apologies if it's not the same where you are

My wife and I are comfortable. Both of our parents have worked in banking and taught us budgeting beyond what school taught us.

Keeping a steady well paying job is key. Sadly, there are so many people who no fault of their own can't get well paying jobs or live in areas where well paying jobs are rare.

Not great, but I might be able to cover a grand in an emergency.

Not sure if youre only asking Americans, but in case this is for everyone:

I'm doing pretty well.

Could probably scrape by for a year if my wife and I both lost our jobs.Mainly lucked into success:

My boss from a summer job when I was in college knew the boss of an internship I was applying for, and put in a good word for me.

They hired me upon graduation, but went under shortly after, however a large company was on a hiring spree right at that time and I landed a job there with a hefty pay bump.

Then I got laid off there right as a local startup was on a hiring spree to increase their valuation because they were looking to be acquired by a major high-tech company, and they hired me, again with a hefty pay bump.

They got acquired, and I started working on a team based on San Francisco. Because wages here were so much lower than the bay area, they were throwing raises at me because it was pennies to them.

I've been there for over 10 years.As long as AI doesn't make my job redundant, I'll be good for the foreseeable future.

Barely surviving, but not from everyday expenses. Got two kids in college and this year FAFSA decided not to give any help to anyone so all expenses are on me.

I do well enough to comfortably support my wife and me. I have a retirement plan, put a small amount into saving, and don't buy things on credit (besides to pay them off immediately for rewards points). I have paid off my car and it should last me a good long while. I do have student loans outstanding but I pay those down and my work provides a stipend each month that effectively doubles my payment on that. I have some small investment accounts to play the stock market, but not life-changing money. We have plenty of money leftover after the mortgage to live just as comfortably as I would like.

This all being said, I am an outlier in the current economy. Most are paid too little for too much work and I would happily pay more for most products if I thought the money was going to the employees, but I know they are given the smallest amount possible.

It's not remotely crazy, and I have lived there. I had times where I foraged for berries and plants for food, and was lucky enough to know how and where to do so. That was a long time ago, before wages stagnated and inflation went bananas. I'm surprised more people aren't starving to death today, just looking at the numbers.

It's a little crazy when we're talking about half of the population.

Look up prices for housing, food, etc. in your area and compare that to full time at minimum wage. Then consider a lot of companies only hire part-time and not full time. Then consider minimum wage is still the federal $7.25 in a lot of the country. See how that math looks.

After school I had one week of cash left when I got my first job. I moved to a tiny town to work in the mining industry. Pay to cost of living is very good. I've always been careful with money and dislike shopping.

I save about 50% annual income. This is piled up in various investments. I can retire before 40.

I have about 1 year worth of expenses in cash I can access tomorrow. I try to keep at least 3 months but I'm squirreling away extra for known upcoming expenses.

It is crazy given my healthcare costs are 2k. I pretty much have a monthly nut of 6k and my wife and I do not live a lavish lifestyle oh and I won't be able to work much more before I will have to figure out retirement. I will be in ruin if I can't produce thousands a month.

Could be better.

No debts, but I burned through all my work coping mechanisms on the way to paying them off, burned out badly and now I can barely look after myself, let alone do things for someone else.

Luckily, if you can call it luck, at least one of the benefits agencies of my country (can't really say government as they don't change much if at all when the government does) agrees with my self-assessment and is providing me a pittance to live on. If I still had a mortgage (or rent) though, I'd be f--ked. Then again maybe I'd qualify for some other kind of assistance. I don't exactly want to have to find out.

One of the other agencies largely implied that all I needed was a nagging wife and I'd be A-OK. Yeah, no, that's not how mental illness works. Pretty sure at least one of us would end up in the ground. Probably just me, because I don't think I could bring myself to harm anyone else.

But, to drag this back on topic, I have some funds put by for emergencies, which might cover me a couple of times. After that, well, I try not to think about it.

I get job contracts for a few months at a time. Sometimes there are months when I'm unemployed, and those are hard on my savings. I used to do just fine, but this year has been very difficult and my normal savings are pretty much gone. (I still got some in funds/investments though.) So basically, I had a buffer but I had to use it, and now I have nothing. I guess it's because of the rise in prices? I don't "waste" money on frivolous things like I might have in the past, but it's only getting more and more difficult. Add to this student loans. I wouldn't have €1000 to spare for an unexpected expense. I am really angry at society, to be honest. If the job market wasn't so ass, I wouldn't have to deal with these short contracts.

we're fiiinnneeeee. could be better

Average at best.

Started paying off debt, saving, and investing consistently over 25 years ago. It has really worked out, and my wife and I are more financially secure than most. Even still, we're one health crisis away from potential bankruptcy, because we live in the United States.

I'm tied down by one financial anchor and have opted to add two more smaller ones on top of that for giggles. I live very comfortably paycheck to paycheck, if I need to save for anything I can fairly easily put away around 3k a month. I can afford a random 1k expense without issue, currently anything above 2k would be a bit tougher, but still manageable.

Are you saving for retirement?

Money is like water, you need some amount but more is not better. The smarter you are the less you need and the easier it becomes to always have plenty.

It sounds crazy to you because you have apparently had success handed to you through no work or special virtue of your own. Maybe get out of your comfy bubble a bit

They may be in a comfy bubble but that doesn't necessarily mean that haven't worked hard and/or been lucky. Kind of a harsh assumption about a stranger.

Such a privilege to be born plumber